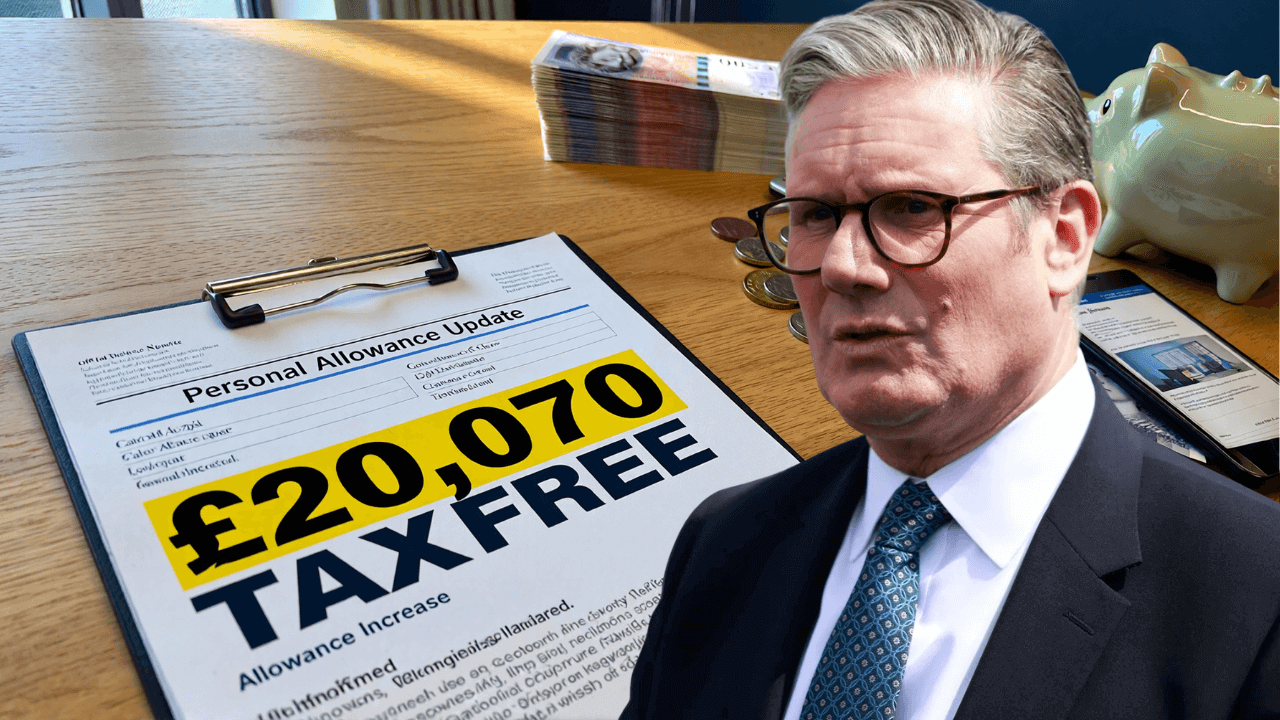

Taxes play a major role in the financial system of the United Kingdom. Every worker, retiree, and person earning income must follow tax rules set by the government. One of the most important parts of the UK tax system is the personal allowance, which determines how much money a person can earn before they start paying income tax. Recently, many people have been discussing the idea of a possible £20,070 tax-free income level, which has created confusion about whether the government has increased the personal allowance.

Understanding the Personal Allowance

The personal allowance is the basic amount of income that most people in the UK can earn each year without paying income tax. This system is managed by HM Revenue and Customs, which collects taxes and oversees the country’s tax regulations. The personal allowance currently allows individuals to receive a certain level of income from work, pensions, or other sources before tax is applied. Once earnings go above this threshold, the remaining amount becomes taxable according to the applicable tax band.

Why the £20,070 Figure Appears in Tax Discussions

The figure of £20,070 often appears in tax discussions because different allowances can sometimes combine to create a higher level of tax-free income. This does not mean that the official personal allowance has increased to that amount. Instead, it reflects how additional tax allowances, especially those related to savings income, may increase the total income someone can receive before paying tax.

यह भी पढ़े:

HMRC Officially Confirms New Notices for Pensioners With £3,000+ Savings : Full Rules Explained

HMRC Officially Confirms New Notices for Pensioners With £3,000+ Savings : Full Rules Explained

In certain cases, a person with moderate earnings and savings interest may benefit from multiple allowances at the same time. When these allowances are added together, the total amount of tax-free income may approach figures like £20,070.

Role of Savings Allowances in Tax-Free Income

The UK tax system includes specific allowances designed to reduce the tax burden on savings income. The personal savings allowance allows basic rate taxpayers to earn interest on savings without paying tax up to a certain limit. Higher rate taxpayers receive a smaller allowance, while additional rate taxpayers usually do not qualify for this benefit.

Another important rule is the starting rate for savings. This allowance applies mainly to individuals whose regular income is relatively low. Under these conditions, part of their savings interest may be taxed at a very low rate or even zero percent.

How Allowances Can Combine

| Allowance Type | Purpose | Possible Tax-Free Benefit |

|---|---|---|

| Personal Allowance | Income from salary or pension before tax | £12,570 |

| Personal Savings Allowance | Tax-free savings interest | Up to £1,000 |

| Starting Rate for Savings | Reduced tax on savings interest for low earners | Up to £5,000 |

| Combined Potential Tax-Free Income | Example when allowances combine | Around £20,070 |

Why Pensioners May Benefit the Most

Retired individuals are often more likely to benefit from multiple allowances. Many pensioners receive income from the State Pension, private pensions, and savings accounts. Because their income levels may fall within certain limits, they can sometimes combine the personal allowance with savings allowances to increase the amount they receive tax-free.

This combination can help retirees protect more of their savings and manage their retirement income more effectively.

Understanding Tax Codes and Financial Planning

Tax codes are used to ensure that the correct amount of tax is deducted from wages or pensions during the year. These codes are adjusted by HMRC depending on a person’s income sources and allowances. Reviewing tax codes regularly can help individuals ensure they are paying the correct amount of tax.

Although figures like £20,070 may appear in news headlines, they usually represent examples showing how several allowances work together rather than a new universal tax-free threshold.

Disclaimer

This article is intended for general informational purposes only. Tax rules, allowances, and thresholds may change depending on government policy and HMRC updates. Individuals should consult official government resources or qualified financial advisors for accurate and up-to-date information before making financial or tax-related decisions.