Many savers and retirees in the United Kingdom are paying closer attention to tax rules in 2026 as interest rates remain relatively high. Recent discussions about a potential £18,570 tax-free income threshold have created interest among people who rely on savings or pension income. This figure does not represent a new official allowance but rather the result of combining several existing tax rules that protect certain types of income from taxation.

Understanding the Personal Allowance

The Personal Allowance forms the basic foundation of the UK income tax system. It allows individuals to earn up to £12,570 each year without paying income tax. This allowance applies to various forms of income, including wages, pensions, and some savings interest.

For many workers and pensioners, this threshold provides essential financial protection by ensuring that a portion of their income remains tax-free. However, the tax system includes additional rules that apply specifically to savings income, which can increase the total amount of money someone may receive without paying tax.

यह भी पढ़े:

HMRC Officially Announces Plan to Raise Tax‑Free Personal Allowance to £13,570 : New Rule Explained

HMRC Officially Announces Plan to Raise Tax‑Free Personal Allowance to £13,570 : New Rule Explained

How Savings Interest Can Increase the Tax-Free Amount

Savings interest is treated slightly differently from other types of income in the UK tax system. Interest earned from bank accounts, fixed deposits, or building society savings may qualify for extra tax allowances.

These additional rules are designed to encourage saving and help individuals keep more of the interest they earn. When these allowances are combined with the standard Personal Allowance, some individuals may benefit from a higher overall tax-free income.

The Starting Rate for Savings

One of the most important additional protections is the Starting Rate for Savings. This rule allows up to £5,000 of savings interest to be received tax-free. However, this benefit is only available when a person’s other income remains below the Personal Allowance threshold.

If non-savings income rises above £12,570, the available Starting Rate gradually reduces. Because of this rule, individuals with lower pension or employment income are more likely to benefit from the full amount.

Personal Savings Allowance

Another layer of protection is the Personal Savings Allowance. Basic-rate taxpayers can earn up to £1,000 of savings interest each year without paying tax. Higher-rate taxpayers receive a £500 allowance, while additional-rate taxpayers do not qualify for this benefit.

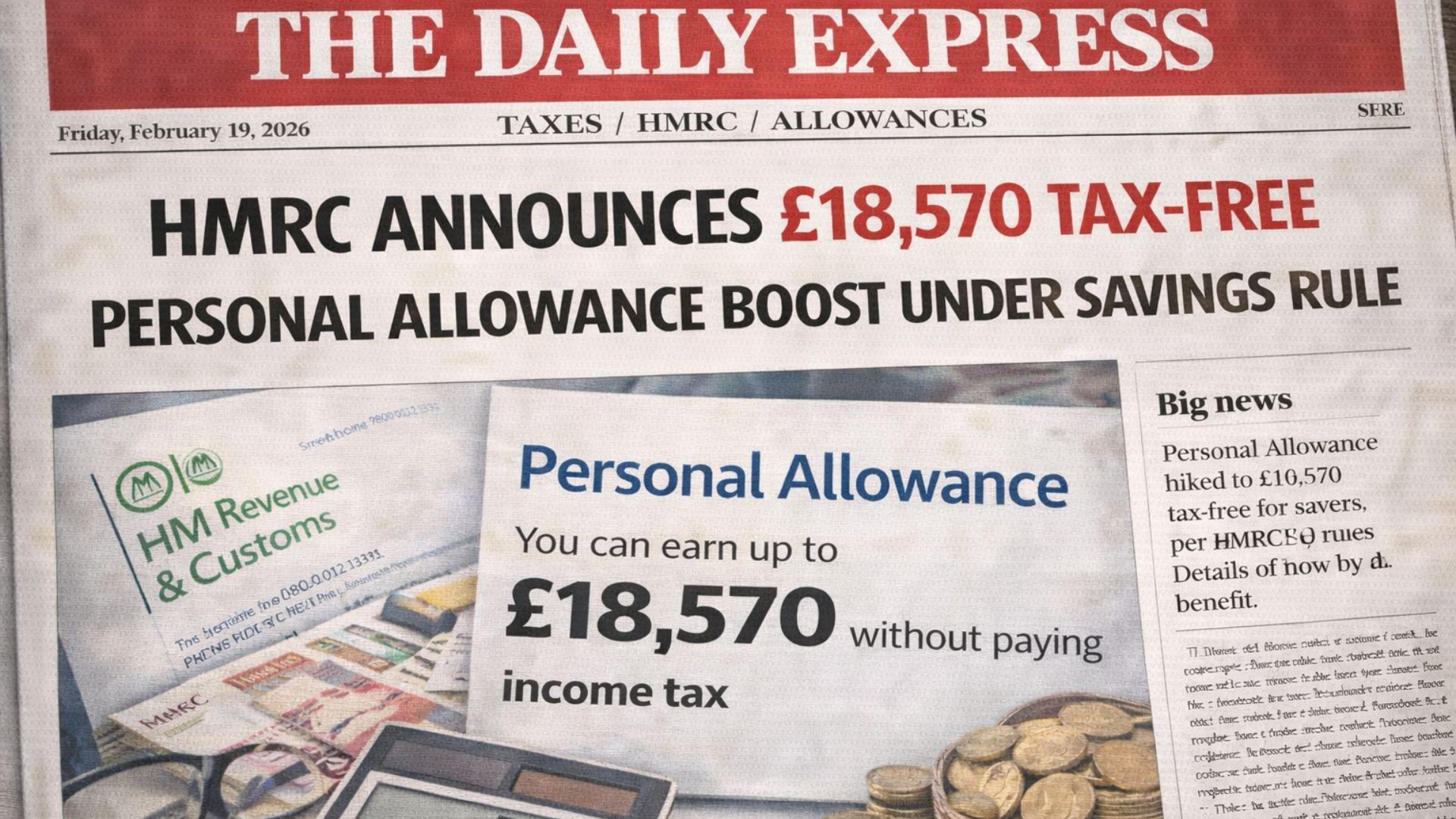

When combined with the Personal Allowance and the Starting Rate for Savings, these rules may allow some individuals to receive up to £18,570 in income before tax applies, provided most of the income comes from savings interest.

Example of How the Allowances Work

| Allowance Type | Tax-Free Amount |

|---|---|

| Personal Allowance | £12,570 |

| Starting Rate for Savings | £5,000 |

| Personal Savings Allowance | Up to £1,000 |

| Maximum Possible Tax-Free Total | £18,570 |

Why These Rules Matter in 2026

With savings accounts now generating more interest than in previous years, more people may approach tax thresholds. Pensioners and individuals with modest incomes may benefit the most from understanding how these allowances interact.

Using tax-efficient savings options such as Individual Savings Accounts can also help ensure that interest remains fully tax-free regardless of income levels.

Conclusion

The UK tax system includes several protections that help savers keep more of their income. When combined correctly, the Personal Allowance, Starting Rate for Savings, and Personal Savings Allowance may allow certain individuals to earn up to £18,570 before paying tax. Understanding these rules can help savers plan their finances more effectively and avoid unexpected tax adjustments.

Disclaimer

This article is for informational purposes only. Tax rules, allowances, and government policies may change based on official decisions. Individuals should verify details through HM Revenue and Customs or consult a qualified financial adviser for the most accurate and up-to-date tax guidance.